Самое актуальное и обсуждаемое

Популярное

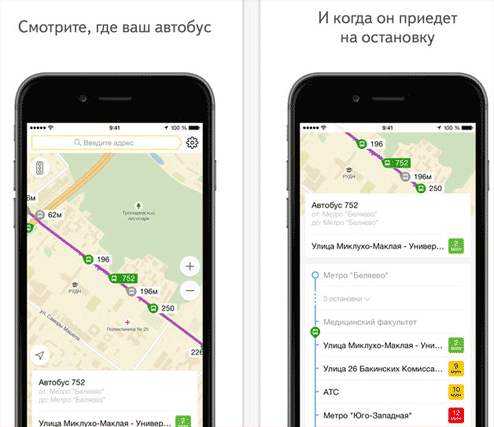

Яндекс транспорт

Возможности Яндекс транспорт для Андроид

Мобильный сервис «Яндекс. Транспорт» содержит абсолютно все...

92

0

0

«яндекс.транспорт онлайн уфа»

Преимущества и недостатки

Стоит отметить, что приложение появилось недавно, поэтом оно не обладает еще...

142

0

0

«яндекс.транспорт онлайн белово»

Маршруты следования с остановками

Сервисное приложение Яндекс транспорт обладает понятным интуитивным...

136

0

0

Яндекс транспорт самара

Яндекс Транспорт онлайн - мобильное онлайн приложение, которое позволяет следить за передвижениями городского...

145

0

0

Какой кредит лучше брать на покупку автомобиля

Оформление автокредита в салоне

Рассмотрим, где лучше взять автокредит – в банке или в автосалоне. В...

111

0

0

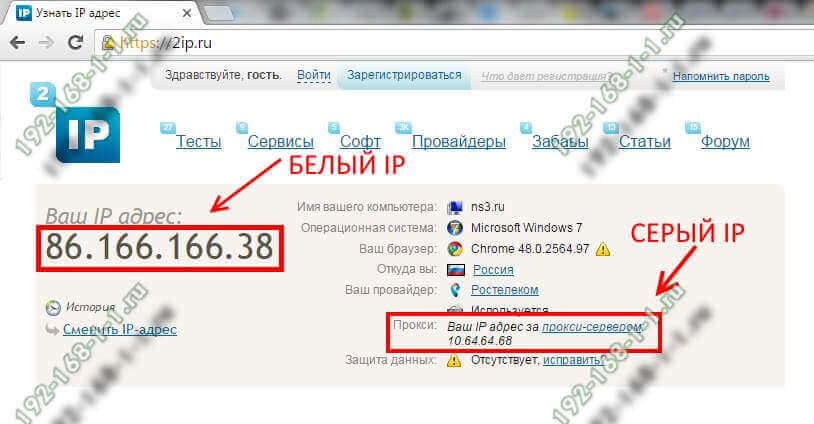

Как определить

Доступ сетке за «серым» IP

Ситуация следующая — имеется некоторый провайдер, который выдает только «серые»...

142

0

0

Лучшие погружные блендеры на 2020 год

Виды котлов

Лучшие мощные стационарные блендеры

блендер погружной рейтинг Kitfort KT-1361

Блендер...

294

0

0

Всё о личном кабинете byfly «мой белтелеком»: как войти, проверить баланс, управлять услугами

Тарифы для юридических лиц и индивидуальных предпринимателей

В соответствии с действующим законодательством...

190

0

0

Полезные советы

Важно знать!

Расширение файла cdw

Формат CDW – чем открыть файлы с расширением CDW, просмотрщик Компас, viewer

CDW – это расширение, которое относится к типу программ для разработки инженерных проектов. Само расширение является форматом...

Читать далее

Газпромбанк: вход в личный кабинет

Гб, мб, кб — это единицы измерения информации, а чем они друг от друга отличаются?

Как открыть эквалайзер в windows 10

Fast boot настройка биос

Финам: вход в личный кабинет

Скачивание программы финам трейд

Рейтинг смартфонов 2020 (декабрь) цена качество

Графики форекс в режиме онлайн

Фьючерс (фьючерсный контракт)

Рекомендуем

0

Лучшее

Важно знать!

Какой samsung galaxy лучше

Лучшие до 20000 рублей

Во многом телефоны ценовой категории до 20000 рублей отличаются от более доступных незначительно улучшенными параметрами и в большей степени приятными и полезными опциями.

Samsung...

Читать далее

Отмечаем человека в тексте поста или записи вк — все способы

Горячие клавиши и комбинации для перезагрузки компьютера или ноутбука с клавиатуры

4 быстрых способа сделать гиперссылку в ворде на всех версиях офиса

Как с компьютера с ос windows 10 можно удалить вторую операционную систему

Способы, как убрать область исправлений в «ворде»

Как убрать замазанное на картинке и вернуться к оригинальному изображению?

Как правильно удалить любую игру и как удалить все файлы от нее. удаление с помощью revo unistaller

Как привязать инстаграм к вк через телефон

В каких айфонах есть nfc модуль

Обсуждаемое

Важно знать!

Непечатаемые символы в word

Знаки абзацев и другие символы форматирования в Word 2010

Одно из основных правил для правильного создания документов в Word – правописание. Не поймите неправильно, так как это не имеет ничего общего...

Читать далее

5 лучших линеек ноутбуков для web разработки в 2020 году

Способы исправления ошибки windows ntdll.dll

Дистанционные онлайн курсы обучения интернет профессиям и заработку через интернет в 2020 году

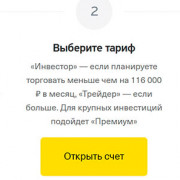

Инвестиции для начинающих

Одноклассники моя страница

Символ переноса строки в excel

Perfect money вход в личный кабинет, регистрация

16 лучших недорогих планшетов 2020

Всё про матрицы монитора: tn, ips, pls, va, mva, oled

Актуальное

Важно знать!

11 доступных движков для тех, кто хочет начать создавать свои игры

скачать приложение для создания игр CryEngine

CryEngine – это кроссплатформенный игровой движок для проектов стационарных платформ (ПК, консолей). Он распространяется по бесплатной модели, с роялти при...

Читать далее

Рейтинг 10 лучших телефонов-раскладушек! новинки 2019

Топ-10 смартфонов samsung 2020, рейтинг по цене/качеству

Что такое рефинансирование кредита и как рефинансировать кредит других банков + лучшие предложения 2019

Как найти среднеквадратическое отклонение в excel

Статусы в вк красивым шрифтом

Где дешевле ипотечное страхование

Support.apple.com/iphone/restore на экране — как убрать

Как в windows 10 открыть параметры папок

Тестовый режим windows 10

Обновления

Без рубрики

IoT взаимодействие с ERP и CRM: максимизация эффективности вашего бизнеса

Без рубрики

IoT взаимодействие с ERP и CRM: максимизация эффективности вашего бизнеса

В современном мире, где технологические решения проникают во все сферы жизни, концепция Интернета вещей...

Без рубрики

Скины CS:GO, CS2, Dota2: разновидности

Без рубрики

Скины CS:GO, CS2, Dota2: разновидности

В мире онлайн-игр, где виртуальная реальность сливается с соревновательным духом, роль индивидуального...

Без рубрики

Заработок в CS:GO и Dota 2: механизмы и возможности

Без рубрики

Заработок в CS:GO и Dota 2: механизмы и возможности

CS:GO и Dota 2, две популярные многопользовательские видеоигры, не только предоставляют захватывающие...

Без рубрики

5 эффективных способов использования телеграм аккаунтов для привлечения и удержания аудитории

Без рубрики

5 эффективных способов использования телеграм аккаунтов для привлечения и удержания аудитории

В наше время социальные медиа играют огромную роль в коммуникации и бизнесе, и одной из популярных...

Без рубрики

Разработка ПО для Astra Linux, ROSA, РЕД ОС, Аврора: экспертное руководство

Без рубрики

Разработка ПО для Astra Linux, ROSA, РЕД ОС, Аврора: экспертное руководство

Разработка программного обеспечения для отечественных операционных систем: преимущества и особенности

В...

Без рубрики

Youtube — новые посты

YouTube — видеохостинг, предоставляющий пользователям услуги хранения, доставки и показа видео. YouTube...

Без рубрики

Банк точка: вход в личный кабинет

Без рубрики

Банк точка: вход в личный кабинет

Интерфейс и дизайн Точка Банк

После успешной авторизации перед Вами откроется главная страница интернет-банка,...

Точка банк: вход в личный кабинет

Точка банк: вход в личный кабинет

Другие способы контакта с банком Точка

Телефонная горячая линия часто не устраивает клиентов банковских...

9 лучших жестких дисков для ноутбуков

Отличия между HDD и SSD

Сколько бы ни было свободного места на диске, его всё равно со временем будет...

Без рубрики

Яндекс транспорт новосибирск

Транспорт онлайн Новосибирск – сервис предоставляющий информацию о маршруте автобусов, трамваев, троллейбусов...

Без рубрики

Яндекс транспорт владимир

Сервис Яндекс транспорт Владимир дает возможность наблюдать онлайн за передвижением общественного транспорта...

Без рубрики

Wix

Шаг3. Финиш Wix.com вход в аккаунт. Свой домен и премиум

http://ваш_логин.wix.com/название_сайта

Это,...

Нашли ошибку, неточность или опечатку в тексте?

Выделите её и нажмите Ctrl + Enter

Выделите её и нажмите Ctrl + Enter